Whitcomb: What Went Wrong; Can’t Make a Decision; Back to the Pequot River?

Sunday, March 19, 2023

“We and the trees and the way

Back from the fields of play

GET THE LATEST BREAKING NEWS HERE -- SIGN UP FOR GOLOCAL FREE DAILY EBLASTLasted as long as we could.

No more walks in the wood.’’

From “An Old-Fashioned Song,’’ by John Hollander (1929-2013), American poet and Yale English professor

“When nature is overridden, she takes her revenge.’’

-- Marya Mannes (1958) 1904-1990, American writer and cultural critic

It’s very pleasant to see the brown and yellow strips of grass along the roads turn a little greener most days, and to hear so many birds singing in the early morning light even with a cold breeze blowing.

We drove deep into downtown Boston last Wednesday afternoon at the height of the rush hour. I was surprised by the lightness of the traffic. The stay-at-home-and-Zoom economy? Nice for drivers but bad news for Boston?

"In finance, everything that is agreeable is unsound and everything that is sound is disagreeable."

-- Winston Churchill (1874-1965), British statesman and writer

“Never before in history {since the Crash of 2008} had so many asset price bubbles inflated simultaneously. But then, never before in history had interest rates around the world sunk so low.’’

--- Edward Chancellor, in The Price of Time: The Real Story of Interest (2022)

The Feds, fearful of a contagion across the banking sector, felt that they had little choice but to extend Federal Deposit Insurance Corp. (FDIC) coverage to depositors in the closed Silicon Valley Bank (SVB) and Signature Bank with accounts of over $250,000, which was supposed to be the official insurance limit. A lot of those plus-$250,000 accounts include well-heeled individuals and companies, especially venture capitalists and tech executives.

More than 85 percent of SVB’s deposits were in accounts with over $250,000! Those customers started a run on the bank that led to the crisis. But now they’re just ducky. The money to make these depositors whole comes from fees that banks pay into the FDIC fund.

The proximate causes of these banks’ collapse after panicky runs on them included that the banks’ managers guessed wrong on interest rates, and had inadequate risk analysis and supervision. And SVB, which had grown too fast, in particular should have had a more diversified customer base; it was too concentrated in the sometimes manic tech and start-up sectors. And a loosening of bank regulations, after heavy lobbying under the Trump administration, also made these banks riskier.

That reminds me of the loosening of railroad-safety regulations under the same regime that may have played a role in the disastrous Norfolk Southern Railroad derailment in East Palestine, Ohio, and the loosening of financial regulations during the George W. Bush and Clinton administrations that helped lead to the Crash of 2008 and the Great Recession.

It’s a pattern:

A crisis spawned by too-light regulation leads to new regulations. A few years pass and people forget (or try to forget) the crisis. Then heavy lobbying by the regulated businesses, particularly effective with Republican lawmakers, leads to removal, or at least weakening, of the regulations, leading to another crisis.

Perhaps the inspectors at the Federal Reserve Bank of San Francisco should/could have caught Santa Clara, Calif.-based SVP’s swelling problems before they got to the crisis point, but maybe the Fed needs more staff. Ditto the Federal Reserve Bank of New York and Signature Bank, which had too many depositors into crypto. It’s too early to know if there was fraud, such as cooking the books, at the banks as opposed to just incompetent and/or unlucky management.

That Silicon Valley Bank executives were selling lots of their stock in the institution before its collapse doesn’t raise the trust level. Smells like insider trading.

But some of the problems is depositors’ and investors’ failure to carefully investigate and monitor the institutions where they put their money and take responsibility – and the hits -- for their deposit decisions. That’s partly, again, because many believe that the government will bail them out, at least partially. This shielding from responsibility is a dangerous thing for a capitalist economy, in which the discipline of pain from bad decisions, as well as rewards for good ones, is needed, lest everything blow up in a speculative frenzy.

Meanwhile, social media, by spreading incomplete and/or erroneous information, can make everything worse.

Anyway, to investors and depositors: Diversify, diversify! And remember that even government debt is not always the best investment.

But maybe I’m too pessimistic. Consider that in Massachusetts, all bank deposits over the official FDIC $250,000 limit are insured by something called the Depositors Insurance Fund (DIF). State law requires all banks and credit unions to pay premiums into this fund.

No depositors at Massachusetts banks have lost money from runs since 1934 because of the fund. And bank failures are very rare in the Bay State, with, for example, only one institution, Butler Bank, in Lowell, collapsing in the 2008-2009 financial crisis.

Some of that good story is probably due to New Englanders being warier of speculation than the high rollers elsewhere.

Some pointers on protecting your money in banks:

See right-winger go to “responsible’ to try to help calm crisis:

Can’t Make a Decision

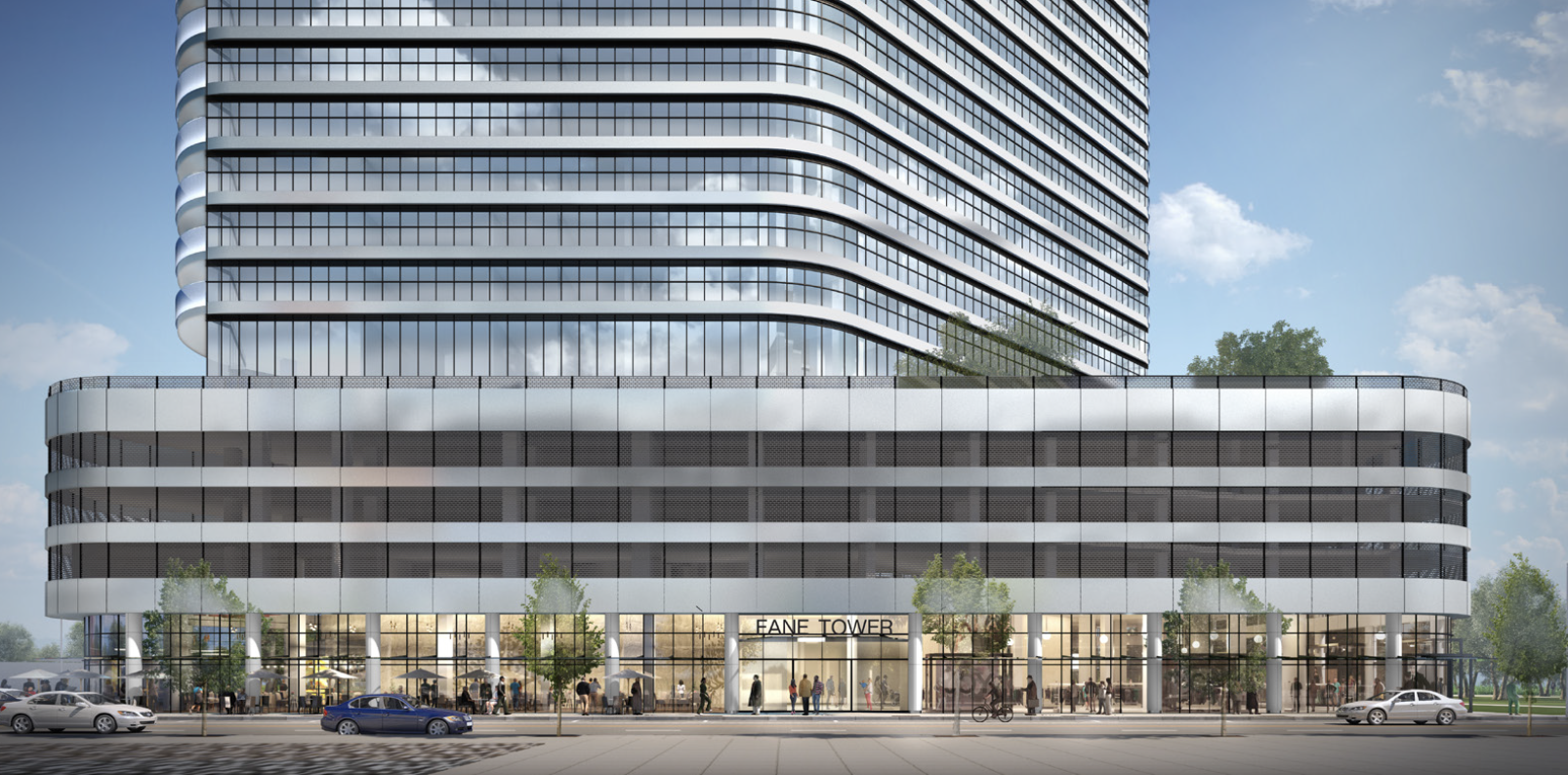

The demise of developer Jason Fane’s plans to build a skyscraper in Providence’s Route 195 Redevelopment District was no surprise, given rising interest rates. The rates were a lot lower in earlier chapters of his saga.

But what has most struck me is how difficult it is to get clear and timely rejection or approval of such big projects by Rhode Island public officials. Mr. Fane’s group proposed the project way back in 2016. Since then, it has ground through layer upon layer of regulatory review.

Rhode Island has long had the reputation of being a tough place to build anything big. Some of the problem is that the review process seems set up to ensure that no individual has to take responsibility for making key decisions. It’s what my friend Philip K. Howard wrote about in his book The Rule of Nobody.

Whatever you think of the Fane project, aesthetically and otherwise, you have to realize that the process that ended with the project’s exit was so long and convoluted that it was a warning to other big developers: “Abandon all hope ye who enter here.’’ And until a proposed project is approved, rejected or just abandoned by a developer, the proposed building site usually can’t be used for anything else.

Maybe the Fane site could become a pasture for cows, sheep and goats to produce cheese. Or a petting zoo with llamas.

I’d like to hear more about NextEra, the corrupt Florida company that will provide electricity to seven Rhode Island communities. They’re promising lower rates than Rhode Island Energy’s for six months starting in May, but it would be an understatement to say that public officials’ explanation of the deal is opaque.

A little background:

New Way to Warm Swimmers

I love this. An English tech startup called Deep Green has installed a small data-processing center under an indoor swimming pool in Exmouth and is using warmth from it to heat the pool.

Data-processing centers give off a lot of heat, which is usually wasted. And swimming pools require a lot of energy to be kept comfortable, which for most people is plus-80F. What else could be heated by these centers?

Paper vs. Screens

Students, faculty members, and staff are upset about the plan of the Vermont State University system (not to be confused with the University of Vermont, whose Burlington campus is run separately) to remove all but about 30,000 of 300,000 books from its libraries to save money on librarians’ salaries, storage space, etc., in the face of a budget deficit. The idea is to focus much more on digital reading.

But reading on a screen and on paper are not the same. Studies have shown that you retain and comprehend material read on paper (reflected light) better than on screens. And reading, especially more than a screen’s worth, is usually a lot easier on eyes when the text is on paper.

https://hechingerreport.org/evidence-increases-for-reading-on-paper-instead-of-screens/

VTDigger, the excellent online news service, reports:

“Under the new plan, Vermont State University, or VTSU, ‘will maintain volumes that have been accessed or checked out between January 1, 2018 and December 31, 2022 and have been deemed academically valuable by the academic department chairs and the Provost.’’’

This isn’t a fair assessment of book usage! Much of the period coincided with the worst of the pandemic.

“VTSU will also keep a small collection of ‘popular, casual, reading books’ and children’s books in the libraries, administrators wrote. Community members will be able to access those books through a ‘take-a-book, leave a book’ honor system.”’

We can understand the financial pressures, but getting rid of so many books is a blow to education.

Trying to Bridge a Name Change

There’s a dispute possibly brewing between the Mashantucket Pequot Tribal Nation, on the east side of the Thames River, in eastern Connecticut, and the Mohegan Tribal Nation, on the west side. Both tribes, best known for their huge casinos, want the river to have a Native American name rather than the English colonial one it has, named after the river that flows through London. (Thus there’s New London on the mouth of the waterway, much of which is an estuary.)

The Connecticut General Assembly is considering legislation to make the name more politically correct.

The Pequots want the river to be named, naturally, the Pequot River, a name used by early English colonists until they had it named the Thames in 1658.

But “In the spirit of cooperation, we have reached out to our neighbors at the Mashantucket Pequot Tribal Nation in the hope of discussing a traditional name that would be agreeable to both of Connecticut’s federally recognized tribes,” said Charlie Strickland, chairman of the Mohegan Tribal Council of Elders.

Hit this link:

https://www.cga.ct.gov/2023/TRAdata/tmy/2023HB-05503-R000227-Strickland,%20Charlie,%20Chairman%20and%20Justice-Mohegan%20Tribes%20Council%20of%20Elders-Opposes-TMY.PDF

This endless name changing is getting tedious. There’s apt to be pushback, as there has been in New York City since 2008, when the Triboro Bridge was renamed the Robert F. Kennedy Bridge. Most people still call it the Triboro.

French vs. Reality

Many French people have been angrily demonstrating against the increase in the country’s age for collecting pensions to 64 from 62 to put the system on a steadier fiscal foundation and make the country more competitive, especially within the European Union. The government of President Emmanuel Macron knew that it would take a lot of heat for its action, though it’s the responsible thing to do.

Having more people working longer would, of course, mean more revenue coming into pension funds and delayed payouts. Not to do so would, among other things, necessitate raising taxes.

But the French, as hard-working as most of them are at their jobs, love their long retirements, and it’s very difficult to take away benefits that have been offered for decades. What would happen in the United States if setting a higher age for taking Social Security were attempted?

Well, it happened under Ronald Reagan:

Bear in mind that the French have long enjoyed, and will continue to enjoy, very generous social benefits that most Americans can only dream of – e.g., among the world’s best universal health-care systems, generous child-care and elder-care services, generally strong public education, a dense public-transportation system and four weeks of vacation.

Giles Merritt, in Friends of Europe, noted:

“When Emmanuel Macron warned French voters last summer that they were living ‘in the last days of the Age of Abundance,’ he was derided by some as a prophet of doom and a defender of the rich. France’s president is nevertheless the only politician of stature who seems prepared to warn Europeans of the awkward consequences of longer lifespans and plummeting birth rates.’’

Robert Whitcomb is a veteran editor and writer. Among his jobs, he has served as the finance editor of the International Herald Tribune, in Paris; as a vice president and the editorial-page editor of The Providence Journal; as an editor and writer in New York for The Wall Street Journal, and as a writer for the Boston Herald Traveler (RIP). He has written newspaper and magazine essays and news stories for many years on a very wide range of topics for numerous publications, has edited several books and movie scripts and is the co-author of among other things, Cape Wind.

Related Articles

- Whitcomb: Rooting for That Long-Range Forecast; Affirmative Action for….

- Whitcomb: Sending Schools Back to School; Vote Yes on #1; Eateries; Housing Nimby’s vs. the Economy

- Whitcomb: Long Day of Election Work; Celebrating New England in Flood Zone; Sad Story of Pius XII

- Whitcomb: Thanksgivings; ‘Millionaires Tax’; Private-Equity Healthcare; Crypto Catastrophe

- Whitcomb: List the Investors; Protect Path to the Water; Trump Trouble; Place for RI History

- Whitcomb: Pesky Facts; McMansions, Undermining Ukraine; Medicare Bonanza

- Whitcomb: Downtown Cannibalization? OPEC, Russia Vote Republican; Corrosively Anti-Compromise

- Whitcomb: Drainage Dilemma; Build That, and They Will come; Dining and Sleeping to Montreal

- Whitcomb: Reading Election Entrails; Newport War; College-Rankings Revolt

- Whitcomb: Fixing Immigration; Empty ‘Defunding’ Rhetoric; Electrifying Round Up

- Whitcomb: They’re Not Overpaid; Media Herd Mentality; Socialist Sunshine State

- Whitcomb: Old Songs; Rx for 2 Hospitals? Jettison Jones Act; World Cup Window on the World

- Whitcomb: Republic of Racket; Warmer Than You Thought; Repelling Roads

- Whitcomb: Theology and Catastrophe; Gasoline-Tax Idea Looks Sillier; Switch to Tents?

- Whitcomb: Working and Drinking; Better Than S.F.; Shell Game Not Over; Unions vs. Democracy

- Whitcomb: Fane Decision; Anti-Business GOP; ‘Junk Fees’; Green Lights for Putin

- Whitcomb: Cicilline’s New Job; Carter’s Career; No Bottom; ‘Nightlife Economy’

- Whitcomb: Healthcare Quandary; Tax ‘Em, Then Untax ‘Em; Anonymous Reports; Politics Is a Drag

- Whitcomb: Closeups in the City; R.I. as Mass. Satellite; Energizing Energy News; Guns for Tots

- Whitcomb: AI and the Real You; Clinical Capitalism; Documents Drama, Cont.; Town/Gown; Jan. 6

- Whitcomb: Our Future Fuel? Housing Help in Newport; Rewilding Suburbia; Go Aluminum

- Whitcomb: Breaking Camp; the Cons Go On; China, U.K. Woes; McKee Right

- Whitcomb: Closed Churches for Homeless; A Serious Immigration Bill; Rep. George Santos (R-Moscow)?

- Whitcomb: Time for Tossing; Linc Almond; Europe’s Heat Wave; State Lottery Losers

- Whitcomb: America Fuels Mexican Violence; Primary Problem; Ivy League Price-Fixing? Perry Mason