Time redemptions to take full advantage of the recent 6.48% variable rate.

By David Enna, Tipswatch.com

First off, before I start talking about redeeming investments in U.S. Series I Savings Bonds, let’s take a moment to ponder just how worthwhile I Bonds have been as an investment over the last several years.

Back in late 2020, before U.S. inflation started surging, I Bonds had a six-month composite rate of 1.68%. That might not sound exciting, but at the time a 13-week T-bill was paying 0.11% and a 10-year Treasury note, 0.68%. The I Bond’s fixed rate of 0.0% was a whopping 83 basis points higher than the negative real yield of a 10-year TIPS.

And then, when inflation began surging into early 2022, the I Bond got a sensational six-month variable rate of 9.62%, towering over the yields of a 13-week Treasury bill (0.85%) and 10-year Treasury note (2.89%).

Through the dire period of pandemic-induced ultra-low interest rates, I Bonds delivered solid returns, tracking U.S. inflation as it soared higher. Investor demand also soared, causing the TreasuryDirect site to crash in October 2022 as the 9.62% rate was about to expire.

In my opinion, I Bonds remain a worthwhile, simple-to-track long-term investment, ensuring your savings will grow tax-deferred with future inflation. But if your investment timeline is shorter-term, you may want to shift money into Treasury bills, where the nominal returns are now 100+ basis points higher. Even if you are investing longer-term, you may want to look at Treasury Inflation-Protected Securities, where real yields are now 70+ basis points higher than the I Bond’s current fixed rate of 0.9%.

I know there are a lot of investors who jumped into I Bonds in October 2022 to get the 9.62% variable rate for six months, followed up by 6.48% for six months. That was a smart move. But now, those I Bonds (which have a fixed rate of 0.0%) are transitioning to a variable rate of 3.38%, well below the market for nominal Treasurys.

Create a strategy

Redeeming I Bonds is a tricky transaction, because an I Bond must be held for 12 full months and then there is a 3-month interest penalty on I Bonds held less than 5 years. Get this wrong and you could lose 3 months of 6.48% interest, or more. For those I Bonds, the best strategy is wait a full 3 months after the 6.48% rate has completed, then redeem early in the next month. That way the penalty will apply to the 3.38% rate.

Here is a guide to the optimal redemption dates for I Bonds purchased since October 2021:

If you bought in October 2021

Your I Bond has a fixed rate of 0.0% and is a candidate for redemption.

- It earned 3.54% (annualized) from October 2021 to March 2022

- 7.12% from April to September 2022

- 9.62% from October 2022 to March 2023

- 6.48% from April to September 2023

- 3.38% from October 2023 to March 2024.

- Optimal redemption date: Jan. 1, 2024.

If held until April 1, 2024, this I Bond will have earned an average annual return of 6.01%.

If you bought in November 2021

Your I Bond has a fixed rate of 0.0% and is a candidate for redemption.

- It earned 7.12% (annualized) from November 2021 to April 2022.

- 9.62% from May to October 2022.

- 6.48% from November 2022 to April 2023

- 3.38% from May to October 2023

- Optimal redemption date: Aug. 1, 2023

If held until Nov. 1, 2023, this I Bond will have earned an average annual return of 6.64%.

Purchase in December 2021: Optimal redemption date is Sept. 1, 2023.

Purchase in January 2022: Optimal redemption date is Oct. 1, 2023.

Purchase in February 2022: Optimal redemption date is Nov. 1, 2023.

Purchase in March 2022: Optimal redemption date is Dec. 1, 2023.

Purchase in April 2022: Optimal redemption date is Jan. 1, 2024.

If you bought in May 2022

Your I Bond has a fixed rate of 0.0% and is a candidate for redemption.

- It earned 9.62% (annualized) from May to October 2022.

- 6.48% from November 2022 to April 2023

- 3.38% from May to October 2023

- Optimal redemption date: Aug. 1, 2023

If held through Nov. 1, 2023, this I Bond will have earned an annual average return of 6.48%.

Purchase in June 2022: Optimal redemption date is Sept. 1, 2023.

Purchase in July 2022: Optimal redemption date is Oct. 1, 2023.

Purchase in August 2022: Optimal redemption date is Nov. 1 2023.

Purchase in September 2022: Optimal redemption date is Dec. 1, 2023.

Purchase in October 2022: Optimal redemption date is Jan. 1, 2024.

If you bought in November 2022

Your I Bond has a fixed rate of 0.4% and is not a good candidate for redemption if you are holding any other I Bonds with a fixed rate of 0.0%. Redeem those first. For this next series I am using the term “potential” redemption dates instead of “optimal” because the 0.4% fixed rate makes these attractive long-term holdings.

In addition, all I Bonds must be held for 12 months before they can be redeemed. For this series, your future redemption decision may depend on the I Bond’s new variable rate, which will be reset on Nov. 1, 2023.

- It earned 6.89% from November 2022 to April 2023.

- 3.79% from May to November 2023.

- Potential redemption date: Cannot be redeemed until Nov. 1, 2023.

If held through Nov. 1, 2023, this I Bond will have earned an average annual return of 5.33%.

Purchase in December 2022: Potential redemption date is Dec. 1, 2023.

Purchase in January 2023: Potential redemption date is Jan. 1, 2024.

Purchase in February 2023: Potential redemption date is Feb. 1, 2024.

Purchase in March 2023: Potential redemption date is March 1, 2024.

Purchase in April 2023: Potential redemption date is April 1, 2024.

If you bought in May 2023

Your I Bond has a fixed rate of 0.9% and it is not a candidate for redemption. This is an excellent long-term holding. If you need the money and have any other I Bonds with a fixed rate of 0.0%, redeem those first.

In addition, all I Bonds must be held for 12 months before they can be redeemed. For this series, your future redemption decision may depend on the I Bond’s new variable rate, which will be reset on Nov. 1, 2023.

- It is earning 4.3% from May to October 2023.

- The variable rate will reset on Nov. 1, but the fixed rate will remain at 0.9%.

Purchase in June 2023. Potential redemption date is June 1, 2024.

Purchase in July 2023. Potential redemption date is July 1, 2024.

Purchase in August 2023. Potential redemption date is Aug. 1, 2024.

Understanding the pattern

The optimal redemption pattern is consistent for all I Bonds, no matter the year they were purchased. If you bought an I Bond any time within the last 5 years, here are the current ideal times to consider redemptions to minimize the three-month interest penalty:

- January: After Oct. 1, 2023

- February: After Nov 1, 2023

- March: After Dec. 1, 2023

- April: After Jan. 1, 2024

- May: After Aug. 1, 2023

- June: After Sept. 1, 2023

- July: After Oct. 1, 2023

- August: After Nov. 1, 2023

- September: After Dec. 1, 2023

- October: After Jan. 1, 2024.

- November: After Aug. 1, 2023

- December: After Sept. 1, 2023

Here is a chart I created for an article in November 2022 that demonstrates why the optimal redemption dates fall back six months for I Bonds purchased in May and November, when the new six-month variable rate is reset:

What about older I Bonds?

You may want to redeem older I Bonds, held more than 5 years with fixed rates of 0.0%. Of course, there will be no redemption penalty, so you simply want to make sure to complete the full six months of the 6.48% annualized variable rate, and then redeem early the next month. (You earn no interest on an I Bond you didn’t hold through the last day of a month.)

For example, let’s look at purchases for each month of 2017 (the same pattern would hold for other years, but make sure the I Bond truly has a fixed rate of 0.0% before you redeem). Some months are ready to redeem right now, but for some others you will want to wait to complete the 6.48% rate.

- Purchased January 2017. Redeem July 1, 2023.

- February 2017. Aug. 1, 2023.

- March 2017. Sept. 1, 2023.

- April 2017. Oct. 1, 2023.

- May 2017. May 1, 2023.

- June 2017. June 1, 2023.

- July 2017. July 1, 2023.

- August 2017. Aug. 1, 2023.

- September 2017. Sept. 1, 2023.

- October 2017. Oct. 1, 2023.

- November 2017. May 1, 2023.

- December 2017. June 1, 2023.

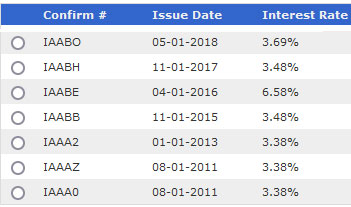

One caution: When you go to redeem an I Bond in TreasuryDirect, finding the correct month-of-issue can be difficult. From your account’s opening page, click on the Series I Savings Bond radio button near the bottom of that page and click “submit.” Then you will see your “Current Holdings” and issue dates.

For an older I Bond — held more than 5 years — look for the I Bonds listed with an interest rate of 3.38% — the current variable rate combined with a 0.0% fixed rate. That older I Bond is safe to redeem.

In this example, the lower three I Bonds have a fixed rate of 0.0% and have transitioned to the 3.38% interest rate. Those can be priorities for redemption. The others all have a better fixed rate and one is still paying 6.58%. Those are not the ones to sell first.

A reminder about taxes

When you redeem any savings bond, you are taking money out of a tax-deferred investment and you will immediately owe federal income taxes on your interest earnings. If you are doing a large number of redemptions, you could climb into a higher tax bracket or potentially trigger Medicare IRMAA surcharges.

An example: Let’s say you want to redeem $10,000 in an 0.0% fixed rate I Bond issued in May 2017. As of August 1, that I Bond had a value of $12,400, so if you redeemed today that decision would create taxable income of $2,400. If you are in the 22% tax bracket, the federal income tax would be $528.

You can easily check the current value of any I Bond using TreasuryDirect’s Savings Bond Calculator (which will automatically subtract 3 months interest for I Bonds held less than five years) or at EyeBonds.info, an accurate and extremely useful resource for information on I Bonds and TIPS.

Final thoughts

I am not advocating selling out of I Bonds. These savings bonds remain a very safe way to push inflation-protected cash into the future.

But I also don’t see the need to hold I Bonds for 30 years. As you enter retirement years, it makes sense to consider redeeming I Bonds to supply cash when you need the money. Or, for people with a shorter-term view, to switch to a more attractive near-term investment like a 1-year T-bill. Or, to use proceeds from a 0.0% I Bond to roll into a new I Bond investment with a 0.9% fixed rate, possibly using the gift box strategy.

As you ponder redemptions, remember to first target I Bonds with 0.0% fixed rates. And for I Bonds held less than 5 years, wait until you’ve transitioned into the 3.38% interest rate for a full three months.

If you got this far … This article contains a lot of numbers, months and years, subtracting six months here and not there. If you spot any errors, post them in the comments area and I will thank you and make a fix.

• I Bonds: A not-so-simple buying guide for 2023

• Confused by I Bonds? Read my Q&A on I Bonds

• Let’s ‘try’ to clarify how an I Bond’s interest is calculated

• Inflation and I Bonds: Track the variable rate changes

• I Bonds: Here’s a simple way to track current value

• I Bond Manifesto: How this investment can work as an emergency fund

* * *

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear. Please stay on topic and avoid political tirades.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

David, any chance of getting an update on when to take the “exit ramp” on I Bonds purchased after May 2023? Thanks

If you purchased in May 2023, you can’t redeem until May 1, 2024. However, those I Bonds have a fixed rate of 0.9% and are paying a composite rate of 4.86%. I don’t recommend redeeming I Bonds with a fixed rate of 0.9% if you have other options.

That’s my understanding too. I’d LOVE to swap .9 for 1.3 but even with my 2 people and 3 LLCs, It would take a couple of years. I’m happy having followed your extremely helpful guide, redeemed all my 0 and .04’s, and will be able to redeploy all 5 max contributions to 1.3 in April. (before the May reset). Now in the event that we learn in April that the May-Nov rate will be =/> 1.3, would it make sense to wait until mid-late October to deploy, given that I should easily be able to enjoy 5% plus interest in risk free MM or < 1 year T-Bills?

Pingback: Random thoughts on I Bonds in 2023, 2024 | Treasury Inflation-Protected Securities

David, I have been a regular reader of your blog and an investor in I-bonds since 2001. Generally, I have purchased I-bonds with the intent of putting them on the shelf and forgetting about them, but now that I am retired (age now in the early 70’s) and have more time than money, I am considering tinkering with them just a bit. Specifically, I have a number of I-bonds purchased with fixed rates ranging from 0% to 1.2%, with a number in the 0.0% to 0.7%, with most of those held over 5 years (no redemption penalties). I read this blog on redemption strategy with interest (when it was published in early Aug 2023), and now that the November 2023 reset has been announced with a new fixed rate of 1.3% I am considering “swap” redemptions of both paper and electronic bonds with a fixed rate of 0.7% or less in order to reset these to the new, much higher fixed rate. I understand that while there will be no interest penalties, involve paying income taxes on earned interest, plus lock up the new bond investments for a year + create 5-years of 1 quarter penalties, but by the same token it will lock in the new fixed rate and extend bond maturities as well. What is your thought on this approach, and if you were to redeem the I-bonds perhaps 5 to 10 year TIPs might be a better investment? Thank you.

A couple things to consider: 1) you will owe federal income taxes for all interest earned at redemption — beware of potential tax bracket creep or Medicare IRMAA surcharges — and 2) no matter how much you redeem, you’d still be limited to purchasing $10,000 per person per year. So unless you used the gift-box strategy, you’d be lowering your I Bond holdings. After retirement, it’s hard to raise the cash needed to purchase I Bonds without facing tax consequences, so I understand the idea of rolling over 0.0% fixed rate I Bonds for the new 1.3% issues, this year and next. I personally would hold any I Bonds with a positive real yield.

On TIPS versus I Bonds: There are no purchase limits on TIPS and the real yields are substantially higher so it could make sense to swap I Bonds for TIPS. But I consider them different investments. I Bonds create an inflation-protected stash of tax-deferred savings, risk-free and accessible. TIPS are best held to maturity as part of a year-by-year strategy, targeting maturities. Also, it’s probably best to buy TIPS in a tax-deferred brokerage account, and the I Bond redemptions won’t help fund purchases there.

Spot on!!

I bought in Oct 2021.

You wrote that the optimal redemption date is Jan. 1, 2024.

And if I held until April 1, 2024, this I Bond will have earned an average annual return of 6.01%.

So are you saying that if I wait until April 1 I will have a higher rate of return than redeeming in January or Feb or March?

I don’t understand how you’re using the term “optimal.” My investments in ibonds was purely to park short term cash.

Thank you, this post has been unbelievably helpful.

The idea of the “optimal” redemption date is that you have allowed three months of the 3.38% rate to pass, so the 3-month penalty will be applied to the 3.38% months and not the 6.48% months that ran through September on your I Bond. For you, that will be Oct, Nov, Dec. The idea of the 6.01% April return was if you DO NOT redeem, that will be your average annual return through April 1.

Thank you!

For the I-bonds bought in Oct 2021, 3.38% is paid oct 1st, nov 1st and dec 1st. Why can’t I redeem on dec 1st since the interest is already paid? Why wait until next month?

I also have bonds I bought in March 2022, When I believe I can redeem right now. Will I forfeit one of the 6.48% month interest?

For the Oct 2021 I Bonds, the rate changed to 3.38% in October. Then November, December. On Jan. 1 you will have completed three months at 3.38%. For March 2021, the rate changed in September. Then October, November. On Dec. 1 you will have completed three months.

Thanks tipswatch. That’s what confuses me. Since I have already recieved the last of the 6.48% for the bonds bought in march 2022 (assuming my first interest was in march 2022, not april) on the first of the first of this month – shouldn’t I be able to sell and keep it? Is this a safety measure? The last time I bought I bonds before these two years was in april 2008 when the fixed rate was 1.2% which I am going to hold to maturity. Wish the fixed rate this time was higher. Your prediction was spot on. My plan is to sell these two ibonds for 1.3% ones for this year and next. Thank you for your wonderful blog.

RK, remember that the interest you receive each month is for holding through the previous month. So in October, you receive interest from September. You don’t receive October interest until Nov. 1.

Got it. Didn’t realize it was for prior month. Thanks tipswatch

Thank you for all the info and analysis.

I have i-bonds purchased in Nov18 and Apr19 (with 0.5% fixed rate), and Apr22 (0% fixed rate). The latter was to take advantage of the high variable rate. I will redeem on 1st of January, to minimise the interest loss. For the first two if I redeem them in Nov 1st and April 1st 2024 respectively, I should not have any penalty at all (won’t lose the last 3 months of interest), is that right? At that point, will the value displayed increase by >10% (the last 3 months of interest added)? Because right now the value displayed seems to be the same as I can redeem which must mean that the last 3 months of interest are not included in the figure shown.

After 5 years TreasuryDirect will show the full amount. Before that, it subtracts the last three months.

If you need the cash within the next couple of years, then you should sell your 0% fixed rate I-bonds and put the proceeds into 3- or 6-month T-Bills, which are currently yielding more than 5.4%. It makes no sense to buy new I-Bonds unless you won’t need the cash within the next five years, and even then 5-year TIPS are probably better. Short-term Treasuries offer the best return and your money won’t be locked up for years. I-Bonds were great back in 2021 and 2022, but they are no longer the best deal in town.

Thank you for a fantastic article! I bought in January 2022 and am heavily considering redeeming come October 1st, but curious if there is any reason I should perhaps hold off entirely on redeeming? My thought was that since the fixed rate for this I-bond is at 0.0%, if I redeem in October, I can either buy and get the 0.9% fixed rate (since I haven’t purchased any I-bonds in 2023 yet) before the November rate is announced, or buy once the November rate has been announced. In my head, it seems like a no-brainer to redeem on October 1st, but I wonder if I might be missing anything.

I can see this strategy as being sensible. You will lose three months of interest at 3.38%, but gain a much higher fixed rate. The next variable rate will be known after the September inflation report is issued Oct. 11. One interesting curve ball is that the fixed rate could rise on November 1, so maybe you will want to wait until November 1 to repurchase. No way to tell for sure on the fixed rate, but my feeling is that it won’t go down, and more likely will go up if real yields maintain at current levels.

This article is exactly what I’ve been looking for, thank you.

But I can’t seem to find an answer to; Is gifting an I-Bond a taxable event ?

Gifting to a spouse (who is a U.S. citizen) is definitely not a taxable event. But for everyone else, the gift could be subject to gift tax limitations. Read more here: https://thefinancebuff.com/buy-i-bonds-as-gift.html#htoc-gift-tax-form-709

A follow-up,

Is the 3 mo. interest sacrifice lost at the time of delivering a gift or when my wife redeems? I’m assuming it’s not both but likely when it’s delivered and it’s not taxable until she redeems it? Is that correct? I have multiple bonds that should be redeemed before years end. I’m trying to be mindful of taxes.

The terms of the bonds — interest rates, when the bonds can be cashed out, when the interest penalty ends — are set when the bonds are initially purchased. The bonds carry the same terms when they are moved from one account to another, i.e. “delivered.” It doesn’t matter which account the bonds reside in.

If I redeem an I bond, for example, 2 months before the next date on which interest is added to my principal, will I receive the 4 months of accrued interest that had not yet been added to my principal since the last time interest was added to my principal less any early redemption penalties?

Also, on which day of the month is interest accrued? If it’s the last day of the month, then if I redeem on the first day of the next month, I should receive all of the interest of the prior month less any early redemption penalties? Correct?

I Bonds earn interest after each month is completed. So if you redeem on Sept 1, for example, you will receive all interest earned through August. But if you haven’t held the I Bond for 5 years, you would lose interest for June, July and August..

Regarding the “breakeven” discussion, suppose you were debating whether to redeem I Bonds purchased, say, in January 2022 (with a zero fixed rate) and to replace them with new I bonds having a .9% fixed rate. Further suppose that you went ahead and bought the new ones but decided to hang onto the old ones instead of redeeming them. Wouldn’t it take something on the order of 14 years for the value of the new ones to catch up with the then value of the old ones? If so, does this enter into a decision to replace zero fixed rate bonds with .9% fixed rate bonds?

It’s complicated, isn’t it? OK, that $10,000 I Bond purchased in January 2022 is now worth $11,240. If you redeemed today you’d get $11,088 after the penalty. You’d then have $10,000 to buy another I Bond with a fixed rate of 0.9% and $1,088 extra to invest in a 4-week T-bills earning 5.5%. The new I Bond you bought in August would be worth $10,216 on Feb. 1, 2024, and your $1,088 earning 5.5% would be worth about $1,113. So after six months you have $11,329. If you held the 0.0% I Bond instead of redeeming you’d have $11,396 on Jan. 1, 2024. So the breakeven is getting pretty close after just six months, IF you can invest the excess earnings from the I Bond redemption.

Thanks for all of the replies. I should not have referenced “breakeven” in framing my question, because this created confusion. The thought of redeeming a zero bond and replacing it with a .9% bond led me to compare the continued performance of the zero bond (as though I did not redeem it) with the performance of a new .9% bond. Under this hypothetical I am owning both the “old” and the “new” bonds. Now compute the time in the future when the new bond (with the extra .9% yield) will equal the value of the still-performing old bond. I realize that income tax expense for redemption proceeds and alternative investments of redemption proceeds are important considerations in deciding whether to redeem, but I am not there yet.

If you hold onto the 0% Jan-22 bond and purchase the current 0.9% bond in October, the two bonds will have the same value sometime in early 2037, depending on the future variable rates.

Thanks for doing the math. So, if my holding period were less than 14 years, it probably wouldn’t pay to replace a 0% with a .9%.

What you asked was how long it would take for the 0.9% bond to catch up with the Jan-22 0% bond were you to buy the 0.9% bond AND hold onto the 0% bond; that would be approximately 13 years 4 months give or take a few months depending on future variable rates.

If you REPLACE the 0% Jan-22 bond with the current 0.9% bond in October, i.e. sell the Jan-22 bond and use the proceeds to purchase the current 0.9% bond, then you will break even in April 26 (2 years, 6 months) assuming a future variable rate of 3%. If the future variable rate is 2% you will break even in 1 year 9 months; if the future variable rate is 4% you will break even in 3 years 4 months. These calcs do not take taxes into account.

Kevin, when you say “replace a 0% with a .9%”, I’m assuming you are considering either A) keep the Jan 2022 0% fixed bond or B) redeem the Jan 2022 bond on 10/1/23, pay the 3-month penalty, and replace it with a new 0.9% fixed bond. As David noted, you should wait until 10/1/23 to redeem the bond so as to minimize the 3-month penalty… forfeit the Jul-Sep 2023 interest that was only at 3.38% instead of the 6.48% interest you earned in May and June.

It’s your money, but if it were mine, I would go with option B if you plan to hold it for more than a year or two. The variable rate component on the replacement bond will be the same as on the Jan 2022 bond, but you’ll get a 0.9% kicker every year on the fixed component. It won’t take long to recover the 3-month penalty. The taxes won’t be too much since you will only have earned interest for 18 months.

I need to remind everyone that when you redeem a $10,000 I Bond with a 0.0% fixed rate, you could be getting $11,000 in cash. You can then buy the 0.9% I Bond with $10,000 (possibly with the gift box strategy) and have another $1,000 to put to work earning 5%+ in short-term Treasurys or other investments. What you lose is the three-month interest penalty. What you gain is a 0.9% fixed rate versus a 0.0% fixed rate. You aren’t going back to zero.

Agreed. If you intend to hold your 0% fixed I bond for more than a couple of years, the only compelling reason to keep it rather than flip it to a new 0.9% fixed I bond would be if it’s an older bond with a lot of accumulated interest and the tax cost would make it prohibitive.

The tax issue is, in my opinion, irrelevant, because eventually (30 years max), we, or our heirs, will redeem the bonds and pay the taxman. Assuming an average variable rate of 3%, $10K of bonds purchased in Jan-22 (0% fixed rate) will be worth $26,176 after thirty years, whereas $10K of the current bond (0.9% fixed rate) purchased in October will be worth $32,056. Sure, we’ll pay more in taxes on the 0.9% bonds but we’ll also pocket a lot more cash.

It’s really quite simple. If you redeem $10K in bonds purchased in Jan-22 (0% fixed rate) and use the proceeds (less the $1,208 in interest, which you can pocket and pay taxes on) to purchase $10K of new bonds in Oct-23 (0.9% fixed rate), then it will take 2 years, 6 months to break even, assuming a future variable rate of 3%.

If the future variable rate is 0%, then it will take 10 months to break even; a future variable rate of 6% will take 5 years, 8 months to break even. The future variable rate would need need to be 14.6% for it to take 14 years to break even.

Bonds with a fixed rate of 0.9% will always outperform bonds with a fixed rate of 0%. The breakeven period depends on the future variable rates: the lower the future variable rates the shorter the breakeven period.

One thing I’ll add about my earlier comment: I didn’t factor in the effect of taxes on the redemption, which would lengthen the break-even period because you’d have less to reinvest elsewhere. Of course, taxes eventually will be due, either way.

In my example, I am factoring in the benefits of reinvesting the $1,088 extra cash you get by redeeming, and putting it into an asset (4-week Treasury) that actually has a higher current yield than the 0.0% I Bond (5.5% versus 3.38%).

The net proceeds in the sale of $1oK of Jan-22 bonds in October 23 will be $1,208 ($11,208 minus $10,000). Here are the breakeven periods if $10K of new bonds are purchased in October and the future variable rates remains 3.0% for different tax brackets:

No tax: 2 years, 6 months

10% tax bracket: 4 years,3 months

12% tax bracket: 4 years, 7 months

22% tax bracket: 6 years

I finally got my spreadsheet together with the help of your “optimum redemption” notes. My question: I have 5 accounts, and have been maxing out since June 2021. I know some of my earlier Ibonds have the .4% inflation factor while my newer ones (bought May 2023 and later, right??) have the .9% inflation factor. Is there a possible strategy advantage, long term, to “cashing out” the .4’s and rebuying the .9’s? (forgive my poetic license on terminology…I’m guessing you’ll understand!) Thank you for your perspective.

If you have already bought the 0.9% I Bonds, you might be at the $10,000 purchase limit for 2023. If so, you would need to use the gift-box strategy to buy more, and that requires a trusted partner, like a spouse. For a rollover strategy, I’d focus on the 0.0% I Bonds first, then consider redeeming the 0.4% I Bonds. (I plan to hold on to my 0.4% I Bonds, however.)

I do believe I’ve maxed out the .9s for 2023. I maxed out five accounts in fact. My question is more about whether to let the 4s and 0s ride or cash them out, pay the tax and then reinvest them into .9s once the New Year rolls around. But of course the first thing that pops into my head (and I think it’s the basis of your reply) is that there’s no guarantee that they will be .9 next time around. I get it now, thank you!

I am adding “telepathic” to your skills… as I read that Bloomberg / Yahoo article last week that you referenced and thought of inquiring about breakeven dates. Thank you for all your insightful info and hard work on this site.

Just wanted to thank you for this article. I am sure it was time consuming to write, and I appreciate your thoughtful work. Well done.

Don’t walk, run from I-bond or treasury investments. Customer service is non-existent. Need to make a change? A trek to your bank or local notary is required to make changes to your account with a ridiculous time to resolve estimate. Better off with bank CD or non-interest bearing account vs this investment! You’ve been warned.

You are talking about TreasuryDirect, not Treasury investments. The entire world buys Treasurys, without ever seeing TreasuryDirect. If you don’t like I Bonds, look elsewhere. But don’t bring a troll attitude to this site.

I am posting this for hoyawildcat, who couldn’t get it to go live. This is a presentation of a breakeven time period that calculates in the future value of a 0.0% I Bond (including future interest) and the time it would take to match that value when starting over with a 0.9% fixed rate.

Re: the breakeven period. In October, I intend to cash in the I Bonds ($10K) I purchased in Nov-21 (0% fixed rate, 3.38% current variable rate) and purchase an equivalent amount at the current fixed rate of 0.9% and a variable rate of 3.38%. Taking into account the three-month interest penalty, my net proceeds will be $1,272.

Applying different future variable rates to my new I-Bonds vs. the old I-Bonds, which can be conceived as average rates for the periods in question, here are the breakeven periods:

0.0% variable rate: Breakeven in Mar-24 (5 months)

0.5% variable rate: Breakeven in Mar-24 (5 months)

1.0% variable rate: Breakeven in Apr-24 (6 months)

1.5% variable rate: Breakeven in Jun-24 (8 months)

2.0% variable rate: Breakeven in Oct-24 (1 year)

2.5% variable rate: Breakeven in Mar-25 (1 year, 5 months)

3.0% variable rate: Breakeven in Oct-23 (2 years)

3.5% variable rate: Breakeven in May-26 (2 years, 7 months)

4.0% variable rate: Breakeven in Dec-26 (3 years, 2 months)

Note that the breakeven period depends on the variable rate: the lower the variable rate the shorter the breakeven period.

Actually, what my posting describes is the time that the new 0.9% fixed rate bonds will need to match the value of old 0% fixed rate bonds were I to hang on them.

Thanks! Ditching mine asap. Fortunately, I can use gift box to buy the 0.9% bonds.

When would you sell an ibond bought on 1/1/22 and /1/21?

For an I Bond bought Jan 2022, the earliest optimal date is Oct. 1. For January 2021, also Oct. 1.

What is best date to sell ibond if purchased on 6/1/21?

After Sept 1 2023

Everyone’s tax situation is different, but with tax rates set to increase significantly on 1/1/26 if Congress does not act, it may be a good strategy to redeem all those 0% IBonds and pay the tax in 2023 -2025 tax years. Depending on your situation, you may be less able to afford the tax in the future when tax rates are higher. Also depending on situation you can replace the 0% Bonds with new ones with 0.9% or higher or could move to Treasuries with that 5.5% yield.

I hope the fixed rate rises, as there is a little bit of FOMO from having bought I Bonds at the start of the year. I already unloaded my tranche of I Bonds older than five years, all with fixed rates of 0.2% or less, and am putting them in short term (4 and 8 week) T Bills until I figure out what to do with them. The 5 and 10 year individual TIPS seem intriguing, even with the interest rate risk on early redemption, although I would need to hold them with a brokerage and not through Treasury Direct. Paying taxes on interest and inflation earned annually doesn’t seem like that big of a deal, especially if you are getting 1-1.5% more annually, although if one were closer to the NIIT or EITC cutoff they might feel differently.

Great article, David. Thank you. I’ve been advising my clients to redeem their 0% fixed rate bonds after 3 months at 3.38%, eat the 3-month penalty, and buy 0.9% fixed rate bonds. The penalty is recovered in less than a year.

In the 8/6/23 comments, you and hoyawildcat both seemed to think the 0.9% fixed rate will hold steady or increase when the new issue comes out in Nov 2023. Do you have any insight into how the fixed rate is calculated? I looked at the history going back 30+ years and it wasn’t clear to me.

I’ve already cashed in my 0% fixed rate bonds, and am trying to decide if I should buy now at 0.9% fixed, or see if the fixed component goes up in Nov.

Phil, how did you come up with a breakeven date of less than a year? According to my calculations, and assuming that the future variable rate remains constant at 3%, it should take at least two years to break even.

Figuring the breakeven period: If you bought in May 2022 and redeemed on Aug 1, 2023, you received $10,820 after a $92 penalty. So jumping from a 0.0% fixed rate to a 0.9% fixed rate would indeed take only about a year to break even. However, you will be paying federal taxes on the interest, which creates a larger cost of switching.

On the fixed rate, I can only speculate and no one knows how the Treasury sets the rate, except that it has confirmed that is does monitor market real yields. Right before the May 1 reset, the 10-year real yield was about 1.26% and today it is about 1.68%. If that trend holds, then I would expect the fixed rate to rise.

Pay me now or pay me later on the taxes. Of course it can vary by individual but paying the taxes now might be a good thing. Tax rates will be going up.

In Sept of2022 I purchased 2 $5000 I bonds and named my 2 late 20’s granddaughters beneficiary’s. I wasn’t planning to ever redeem these I bonds for myself but to leave them until they redeem them after I’m gone ( I’m 86). First question will they have to pay taxes on any gains?

In addition to the above purchase I have been buying $5000. 6month T bills one a month since Nov 22. They redeem automatically. How long should I continue this practice and was it smart to do this as a ongoing investment?

Thanks

Hi David, Thank you for this information. Very helpful. I am new to investing in the US Treasury securities. I figured that I Bonds were a safe place to park some cash instead of just sitting in a bank account at that time that was earning practically no interest. I’ll continue to watch rates as best possible. Try to calculate a best time frame to move into a different US Treasury security.

Take care.

David, I am not sure if it is handy to wait until January of the second next year to liquidate I-bonds purchased in April and October.

Because if you wait until January, you have to take the tax consequences of that year into account as well, not just the previous two years. I’d say: better sell on December 31st than just after New Years.

Could work either way, depending on your income and tax situation for the particular year.

I almost made the same mistake you did… the 6.48% penalty isn’t really 6.48%, because you aren’t saving the whole amount by waiting 3 additional months. You are still going to have to pay the 3.38% if you wait. So your savings by waiting an additional 3 months is the DIFFERENCE between the two rates (6.48 – 3.38), or 3.1%. You can earn much better than 3.1%, so the best return would be selling immediately after the 12 months is up and putting that money in any T-bill earning better than 3.1%.

Best return? You will be giving up three months of 6.48% to get about 5% in a comparable investment. Not a huge deal, I agree, but you can’t find 6.48% short-term T-bills right now. No matter what you do, if you redeem before 5 years, you are giving up 3 months interest.

You’re paying a penalty whether you sell at 12 months or at 15 months. So selling at 15 months only saves you the difference between the two penalties, which is 3.1%. By holding an additional 3 months when you could’ve been earning more than 3.1%, your net is less. Do the math. Run two scenarios side by side where you sell at 12 months and earn 4.75% for months 13-15 vs selling at 15 months if you don’t believe me.

Let’s look at a $10,000 I Bond purchased in August 2022 and redeemed in August 2023. You’d get $10,648. If you waited until November 2023 you’d get $10,820, or $172 more. So you would have to find a $10,000 investment that would pay you $172 in three months. That’s a return of more than 6%. Like I said, the dollar amounts are not life-changing, but you can do a bit better by holding for three months longer.

You are correct! I see my mistake now. You have 3 months of no interest either way, so taking the lower payout early means you have to make an equivalent interest rate to break even. I sold Month 14 and put the entire $10,704 in my core investment account earning 4.75%, so the difference was even less, but holding another month would have in fact have been a few $$$ extra.

Nicely done!

Thanks for the info.

Great article. 👍

For those who are able to manage their AGI (perhaps in retirement), when iBond proceeds are used for higher education the accumulated interest is tax free! MFJ AGI below $156K. See Treasury Direct for details. For those with higher ed costs on the not-too-distant horizon, and large interest accumulations, might be worth delaying redemption.

When thinking about taxes, don’t forget about NIIT, that extra special gift some of us get for earning too much investment income.

I am confused as to why you say that for I-bonds bought in April 2022 the optimal date to cash them in is Jan. 1 2024. I would think that, aside from taxes, it would be Aug. 1 2023. The bond would have had the 3.38% annual rate from May 1, 2023 to Aug. 1, 2023.

Is the Jan. 1 2024 recommendation b/c taxes?

Please clarify.

This is a great question because it gets at a common misconception about I Bonds. When you purchase an I Bond, you get the current composite rate for a full six months, and then after six months the rate changes. So if you bought in April 2022, you got 7.12% for six months, then 9.62% for six months, then 6.48% for six months, and then in October 2023 you will transition to 3.38%. So to wait the three months of 3.38%, you need to get through October, November and December. Then redeem in early January 2024.

wouldn’t it be 6.48% after the 9.62% and before the 3.38%?

Aren’t all your ‘optimal redemption dates’ one month later than need be? Using the example of your above reply, why couldn’t you redeem in December 2023? If you did so, you would be forgoing the Oct, Nov and Dec interest payments and the December was credited on December 1. So even if you redeemed on Dec 1 you would reverse that monthly adjustment. Not a big deal, but it seems like you’re holding for an unnecessary extra month in each case.

I Bonds must be held on the last day of the month to get any interest for that month. So you can buy an I Bond late in the month and get full credit for that month. But when you redeem on any day in a month, you don’t get credit for that month. The April 2022 I Bond in this example will be earning 6.48% through the end of September, then switches to 3.38% in October. So hold October, November and December, redeem on January 1.

Nancy, you are right. I skipped those six months in my response. I fixed my comment. Thanks for catching that.

Gasoline prices have jumped up again. That may affect the August and September cpi reports, having some effect on the next I-bond inflation component.

I’ve been seeing consensus estimates of 0.2% all-items for July. That might be low. Seems like if this gas price trend continues, we will get somewhat higher inflation in August and September.

I thought food and fuel were not part of the CPI equation..

Do I have this backwards ??

Food and fuel are not part of core inflation, but are a huge part of all-items inflation, the number you most often hear reported.

It seems like oil is the item most likely to remain unforgiving of “money printing” because the price is set globally regardless of domestic supply and demand.

Maybe others have also said this, or maybe I am wrong. I am just putting it out here on a whim, but when I reflect upon phrases such as as “fossil fuel economy” and “dollar reserve currency” I feel that oil is the item that the world uses to keep a check on the dollar..

Great work. Thank you. What to do with TIPS etf which keeps paying interest while losing value ?

The TIP ETF has had a very bad stretch, with a total return of -12.2% last year, up 1.6% so far this year. I don’t own it. My guess is that it has been through the worst of this stretch, and future returns could be OK. But then real yields just started rising again. Hard to say.

Thank you

What’s the easiest way to cash in series EE savings bonds issued in 1998 and 1999?

Are these paper EE Bonds? If so, take them to a major bank to cash them. We did this last year with 1992 EE Bonds; did it at Wells Fargo.

David,

Thank you for this and many other informative and useful posts. I am about to redeem paper Ibonds with 0% fixed rates and wonder whether there is an easy way to have federal tax withheld at the time of redemption. I began buying Ibonds in 2000 ( I know, lucky me) and like some other readers will be facing a tax cliff in a few years. For planning purposes I would like to incur the tax in the year of redemption. I’m not currently required to pay estimated tax.

Is there a form to tender to the redeeming bank to request withholding?

I am one of the lucky ones, too, because we bought in the year 2000 also. I haven’t had this question before and I tried a little hunting but could find no information about withholding federal taxes at redemption. Couldn’t fine any information. I recently redeemed some 0.0% I Bonds and I don’t recall seeing a withholding option. One thing you could do, if you have any traditional IRA accounts at a brokerage, is to withdraw the amount of tax you estimate is owed and then withhold the entire amount.

I have done this for other investment earnings, but you actually have to withdraw more from the IRA account, to include the tax on what you are withdrawing as well. I recall having to use my high school algebra to figure out the minimal amount…

Thank you for your reply David. I have continued to seek answers and have found few, curious because one would think the IRS would be happy to be paid early. Two ideas: filing a 1040-es might offer a route even if one is not required to estimate. There must be situations, e.g., a large professional fee comes in unexpectedly, where a taxpayer might want to estimate to avoid penalties the next year at tax time. And, apparently one can elect voluntary backup withholding (up to 50%) in a Treasury Direct account, although seeing the path to do that is not easy. Since this would let the taxpayer anticipate taxes on electronic bonds, one would think there would be some form to allow withholding on paper bonds. Maybe this issue will present more often now that the oldest IBonds will begin to mature in a few years.

Or sign up for an EFTPS account and then you can go online and pay estimated tax anytime.

I would like read more future financial posts.

Loved this, very good information.

Just for clarification: when you say optimal date to cash I-bonds bought Sept. ’22 is this coming Dec., if I were to wait till Jan. 1, I wouldn’t have to pay taxes on the interest until April ’25, so it seems better to wait a month if I’ve already bought I-bonds for ’23. Is that right? The word “optimal” is a little confusing. You mean that date or later, right? Thanks.

Yes, later is fine.

Pingback: Want to exit your I Bond investment? You’d better have a plan. | Treasury Inflation-Protected Securities

Thanks for taking the time and effort to explain redeeming of I-Bonds. I am going to keep the link for this post in my TIPSwatch folder to refer to it when I am ready to redeem our I-Bonds. We are in accumulation stage and have not yet sold any and have no plans to sell any for a long time. Our number one concern is taxes and not the fixed rate.

I wish I had found your blog many years ago. I have a lot of catching up to do in building a TIPS ladder. Although your posts have taught how to buy TIPS in the secondary market, finding the right TIPS is something I need to get better at.

As an immigrant, who lived for 22 years in India, mostly a socialist country, 10 years in Canada, a quasi solialist country, now in the US since 1988, and travelled for business all around, I can say without much reservation that there is no place like the US. Our “innovation economy, coupled with a self correcting system, though seemingly chaotic and scary at times, is the best.

China’s economy is on the mend for the worse, a lot worse than what happened to Japan when they were buying building in Manhattan. No, it is not my wishful thinking.

Now only if the US women soccer team could have scored or blocked one more goal this morning….apologies for over indulgence…..best

For long-term holders, it is essential that they cash in ALL of their 0% fixed rate bonds and buy the current bond (0.9% fixed rate) and the November bond (probably > 0.9% fixed rate), even if they have to take the three-month interest penalty and use the gifting option. The optimal months to sell the old bonds and buy the new ones would be Oct-23 and Apr-24, respectively. Bonds with a positive fixed rate will ALWAYS outperform bonds with a 0% fixed rate, with the breakeven in less than three years after the purchase date.

I was never a fan of the gift-box strategy when it was widely used to lock in the 9.62% rate for six months, because it also locked in the 0.0% fixed rate. Some people bought $100,000 (10 sets of $10,000) in October 2022, and now they will have to spend 5 years unwinding those purchases because of the purchase cap. This year, when I bought the 0.4% fixed rate in April, I said I intended to buy another 2 sets of $10,000 later this year if the fixed rate rose. And I will, and I will roll over two sets of 0.0% I Bonds to do it. I will not redeem them ALL. It seems likely the fixed rate could be the same or higher through April 2024. I might do another set then. Not everyone has a trusted partner to achieve the gift-box swap strategy, though.

Right. I will sell all of my 0% bonds in Oct-23 and Apr-24 and buy new gifted bonds at the higher fixed rates. In the latter case, some of the bonds won’t be delivered until 2027, although the five-year interest-penalty clock will begin May-24.

Correction: The interest-penalty clock will begin Apr-24, not May-24.

I will hold on to my I bonds even with 0% fixed rate. I may redeem my more recent EE bonds though. I do not use the gift box strategy.

Don’t forget, EE bonds are only worthwhile if you hold for 20 years so you get the Treasury guaranteed doubling of value.

When an I-Bond is delivered from the gift box after some interest has been added to its value – say increasing it from $10,000 to $11,208 – does that mean the delivery has exceeded the allowable amount for the recipient for the year? Would the delivery have to be just a partial delivery to stay under the cap? Or is the awarded interest not counted towards the limit?

No, only the original principal counts against the cap.

I have a question for David and everyone reading this. Because of the the limitation of 10K/year of I bond. Would you cash out all 0.0% fixed rate? then rolled over 10K to 0.9% fixed rate and put the rest in 5 years TIPS via secondary market (mature in 2027/2028). Note this will be in the taxable account. Any advise will be appreciated.

I am not a financial adviser. My reaction: If your timeline is five years, then this move makes sense. The negative is that you will forfeit an interest penalty on newer I Bonds and pay taxes on all the savings bond money you redeem. Depending on your marginal tax rate, that could be a factor. But a 5-year TIPS has a real yield of 2.16%, substantially higher than those 0.0% I Bonds. If the I Bond’s fixed rate rises again in November, I will probably roll over some 0.0% I Bonds next year (as I did this month).

I’ve been trying to figure out how and when to cash in those 0% fix rate I bonds since purchasing them since 2011. Patience is a virtue and waiting till November to make sure that the rate is locked in is no problem! Even with the lower interest rates for I bonds, I have been executing the ladder strategy with 13 week treasuries. At first it was nerve wracking not having access to the bulk of my savings but it’s all good now. I know that retirement is at least 10 years (still working) away but learning how to make the future a little more secure helps. Keep on writing and I’ll keep on learning, thanks!!

Thanks for the reminder! Planning to wait until January 2024 to redeem my August and September 2022 I bonds as I expect to be in a lower tax bracket next year. (I should probably do the calculations to see if there’s really much difference.)

So I’d been meaning to do the math on my I-Bonds with 0% real yields and then I wake up to this! Thank you very much–I really appreciate all the helpful posts on your site like this.

David, thank you for the artistry and clarity of this explanation. It is much appreciated!

Thank you so much for your consistently clear and thorough explanations. You are truly a good samaritan.

thank you always for your excellent commentary. Can I assume that if I purchased April 1, 2021 that I should wait until January 2024 or does it no longer matter since it’s paying 3 something now and is over a year old?? So complicated….

I piled into ibonds starting in 2001 on when you could purchase $60K/year. It’s been a good investment and nice tax shelter but there will be a large tax cliff starting in 2031. Not so far away as it used to feel. Guess it’s time to start planning for that but have no idea how to approach it so I’ve been ignoring and that’s probably a mistake at this point?? Don’t want to dump the ones that are paying over 9%. Any advice?

I am in a similar situation with the 2031 tax issue. I think the best I can do is convert as much to Roth as possible to lower RMDs and invest in tax exempt bonds. The 2025 sunsetting of current tax laws will also have an unknown impact.

Depending on your situation, Roths seem wonderful assuming they do not get further tweaked (secure 2.0 and Salt deduction) though I have little confidence in that. I converted about 1/2 my ira slowly over the years before 63. And then, as you say, there is the 2025 sunset. Hard to plan with this level of change. Sadly tax exempts will still impact irma’s. Think I will try to distribute the ibond exit slowly over the next 12 years but maybe the best thing is to either buy a bigger house to shelter what comes out of the ibonds or donate my ira rmd when the time comes. Think i’d rather the money go to charity of my choice vs. general tax fund.

I am thinking of starting a similar strategy next year using my IRA and leaving the I bonds alone for now.

How do you define converting as much to Roth as possible? For me it is up to the limit of the 12% tax bracket. 15% I guess after 2025.

A good starting point for Roth conversions is to calculate the (imaginary) IRA RMD based on your current age and convert that amount to Roth and keep doing that every year until you reach 73, when the actual RMD kicks in.

also keep in mind irma cliffs starting at 63, Medicare has that 2 year look back if it’s relevant. Honestly, i was less scientific, I wanted to have half my 401K in a traditional and half in a Roth and spread the conversion over the years I took early retirement to 63. @hoyawildcat approach is probably more optimal.

For estimating how much Roth I can convert, I use the approach of estimating my incremental tax bracket (including IRMAA and NIIT) with my RMD assuming NO Roth Conversions. I then use that tax rate to see how much converting I can do and hold that rate. I’ve deferred my SS until 70 which will also help. My assumption is also that tax rates will be the same after 2025. It’s still a bit of a swag but the crystal ball can’t foresee what Congress will do.

You’re not talking about converting I Bonds to Roth, are you? I’m also in the same boat with a few I’s coming due in 2031 and trying to figure out the tax implications. I’m not eligible to retire until AT LEAST 2035. Husband & I both work in the public school system, so high AGI is NOT an issue. One child in college, another going in 4 years. Best solution I can come up with is converting I Bonds to 529. Not ideal for 2 reasons – 1. That will greatly lower (or eliminate) their chances of financial aid and 2. I was really hoping to be able to use these bonds for retirement as we’ve already been putting some money in 529’s for the kids but haven’t been able to put as much aside for retirement as we would’ve liked. The only other thing I can think of is to rollover to the 529, after they finish college, then make myself the beneficiary, and transfer what’s left into my IRA…. Thoughts?

As long as you are willing to endure the tax and 10% penalty on the earnings portion, unless you will be using for your own educational expenses.

I Bonds can’t be converted to a Roth. But as you note, they can be converted tax free into a 529 plan, as long as you meet the income limitations. You face some tough choices.

Became intrigued with this. There may be a way, but very restricted. https://thecollegeinvestor.com/41864/529-plan-to-ira/ Appears that the owner of the 529 cannot be the owner of the Roth IRA. Interested in others’ thoughts. May do this for my grandchildren, eventually.

When converting a 529 plan to a Roth IRA under the new provisions in SECURE 2.0, my understanding is that the 529 plan beneficiary has to be the same person as the Roth IRA owner. I don’t believe the 529 plan owner is relevant. I opened 529 accounts naming myself and my wife as beneficiaries earlier this year, with the hope of rolling them to Roth IRAs in 15 years.

I just commented on The College Investor site asking if they meant to say that an owner-beneficiary cannot roll to a Roth IRA for that same owner-beneficiary. I think they were just making the point that the owner doesn’t matter… only the beneficiary.

I have read that the beneficiary cannot have changed for the 15 years leading up to the Roth IRA conversion, so it’s important to start the clock running now. Open those accounts, even if you only deposit the minimum. The amount converted to a Roth IRA can’t exceed the contributions that were made more than 5 years before the distribution, plus related earnings. So start the 15-year clock now by opening the account, and you can wait up to 10 years to start the 5-year clock by fully funding the account.

Here’s an excerpt from SECURE 2.0:

https://www.congress.gov/bill/117th-congress/house-bill/2617/text

“…qualified tuition program of a designated beneficiary which has been maintained for the 15-year period ending on the date of such distribution…”

Phil.some of this is repetitive as I just cut and pasted form my Tax preparer. My gripe is the $35k lifetime limit. Best David C

In SECURE 2.0, signed into law on December 29, 2022, Congress attempted to address this problem. Starting in 2024, beneficiaries of 529 college savings accounts (e.g., children or grandchildren) will be allowed to do a tax-free rollover of up to $35,000 to a Roth IRA.

As usual, however, the “devil is in the details.” Here are those details:

The $35,000 limit is a lifetime maximum.

The Roth IRA must be in the name of the 529 beneficiary – not the 529 owner (if different).

The 529 plan must have been open for more than 15 years. It’s not clear whether a new 15-year waiting period is required when someone changes 529 beneficiaries or if the waiting period that applied to the prior beneficiary can be tacked on. We’ll need further clarification from Congress or the IRS.

Rollover amounts can’t include any 529 contributions (and earnings on those contributions) made in the preceding five-year period.

Rollovers are subject to the annual Roth IRA contribution limit. So, for example, if the Roth IRA contribution limit in 2024 remains $6,500, then no more than $6,500 can be rolled over from a 529 to a Roth IRA in 2024. Further, any actual Roth IRA (or traditional IRA) contributions made by the 529 beneficiary would count against the $6,500 limit. The effect of this rule is that a full $35,000 529-to-Roth IRA rollover would need to be done over several years. It also means that the 529 beneficiary doing the rollover must have compensation in that year at least equal to the amount being rolled over.

By contrast, the income limitations on Roth IRA contributions don’t apply to these rollovers. A 529 beneficiary would be able to do a 529-to-Roth IRA rollover even if she earns too much to make a Roth IRA contribution for that year

Looks like your CPA hit the main points.

Yes, 35k isn’t much, but it’s something. I plan to contribute about 12k now, and hope that it grows to 35k in 15 years. Then convert it to a Roth if I meet the other qualifications. My hope is for the same result as if I were allowed to make a 12k Roth IRA contribution today. I would certainly do that if I could.

If I don’t qualify for a conversion for some reason, I’ll probably change the beneficiary to a family member. Having extra money in a 529 plan isn’t a bad problem to have.

Is the three month early withdrawal penalty tax deductible like a CD?

I haven’t ever sold an I Bond early, so I haven’t seen what actually happens. But I can remember other discussions on this topic that noted the penalty amount is not taxable.

I look at the ibonds I hold now are for the next inflation cycle. You can never build a big position fast enough if you keep cashing in your ibonds. It is a pleasant surprise when inflation is running rampant, that you got a safe investment making money. Do not forget the short-term rates will go away as interest rate drops, and if you switch to long bonds, the appreciated principal will be hammered by rising interest rates. Chasing a dwindling yield is a full time job.

I agree with you on this. If you are in the accumulation phase, it’s better to keep building a stockpile of I Bonds by buying each year and not redeeming.

I am wondering if you feel that it makes sense to not “deliver” gifted I-Bonds in 2024 until after the rates are known in May and November 2024 in the off chance that they again become attractive for purchase since the total for gifted + purchased I-Bonds in any year is limited to 10K.

Could be the right move. No problem in waiting, since the I Bond continues to earn interest.

I’ll disagree – No, doesn’t really make sense, though it probably isn’t that big a deal either way. If rates are attractive in 2024, you can simply repeat the gift box process – buy in 2024 as gifts and deliver those in 2025.

There’s very little difference between I-bonds in gift box and active account. The main one is that redemption/penalty clocks start ticking once they’re delivered. So just for future flexibility, you should usually deliver the gifts as early as possible.

The general principle is that you want the issues you’re most likely to want to sell first to be the ones in your active account while those you’ll likely hold longer are fine in the gift box. This means deliver lower fixed rate first.

I believe that the redemption/penalty clocks start ticking when gift box bonds are purchased, not when they are delivered.

Hmm, that surprises me. I thought delivery was treated like a new purchase for the recipient (it does in terms of yearly purchase limit). If so, that’s another user-friendly policy of Savings Bonds – not only do they allow you to lock in a future year purchase at a high rate, but it comes with a shorter penalty window than for those who actually purchased in that year.

The terms of the bonds — interest rates, when the bonds can be cashed out, when the interest penalty ends — are set when the bonds are initially purchased. The bonds carry the same terms when they are moved from one account to another, i.e. “delivered.” It doesn’t matter which account the bonds reside in.

As hoya notes, the clock starts ticking in the month you place the I Bond in the gift box, not when you deliver it. Harry Sit’s article points this out: “The holding period for cashing out also starts right away. If five months have passed between the time of purchase and the time of delivery, the recipient only has to wait another seven months before they can cash out.”

I plan to deliver what’s in the gift box during a future 0.0% fixed rate period because that’s the time the recipient should be the least interested in buying new issues anyway. If the fixed rate is attractive, I want to buy new ones. If it isn’t, I want to make gift box deliveries.

Post-2009, it hasn’t been unusual for new I-Bonds to have a 0.0% – 0.3% base rate for multiple 6-month terms in a row.

Just don’t let yourself forget about them in the event rates stay high for a while 🙂

What a SPECTACULAR SUMMARY of this topic!!!

THANK YOU!!

Too bad there isn’t a way to get out of I-Bonds and into Treasuries or TIPS without triggering taxes on the I-Bond redemptions……

Thank you so much for this detailed post regarding I bond redemptions. I’m wondering what your educated guess is for the next predicted fixed rate for I bonds?

As of today, I would expect the fixed rate to be higher. Maybe 1.1% or 1.2%. That’s a quick guess but a lot can change before Nov. 1. The good thing about the November 1 reset is that the rate is available in January when the purchase cap resets.

Thanks for your insightful article as always. I always thought it was strange that treasury direct website doesn’t break out the fix and variable rates on your past ibond investment. I’m cashing in 5+ yr-old ibonds that have 0 fix rate and take advantage of the great current fix rate.

Don’t forget your tax situation. I bought intending to hold 5 years when I will be retired and in a lower tax bracket.

Thanks for this careful and thorough guide to selling I-bonds. It’s one more among many of your articles that have lent me confidence to take advantage in my own small way of both inflation-protected and regular Treasury markets. It’s very helpful to see so clearly how holding I-bonds compares to holding other bonds.

Hi. I bought in April 2022 when the rate was 7.12% annually. I believe it was then 9.62%, 6.48%, and now 3.38% annually. Can you tell me the annual average return after compounding if I sell in early Jan 2024? Many thanks.

If this was a $10,000 investment, you should get $11,208 in January 2024, after the 3-month penalty. Your annual return would be about 6.7%.

David, Thank you for this. I am one who piled into I bonds between April and October of 2022 and will be redeeming them monthly as you describe (started this month). At the moment the short end of the yield curve outperforms the long end and rates are probably not done going up. I’ll be putting the funds into a twelve month treasury ladder and rolling them over as long as the curve remains significantly inverted. Once the fed stops raising and the yield curve normalizes I will evaluate the options for locking in those rates for a longer period.