NEWS &VIEWS

Forecasts, Commentary & Analysis on the Economy and Precious Metals

Celebrating our 48th year in the gold business

December 2021

“On Wall Street he and a few others – how many? three hundred, four hundred, five hundred? had become precisely that… Masters of the Universe.” – Tom Wolfe, Bonfire of the Vanities

––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––

The Masters of the Universe and Gold

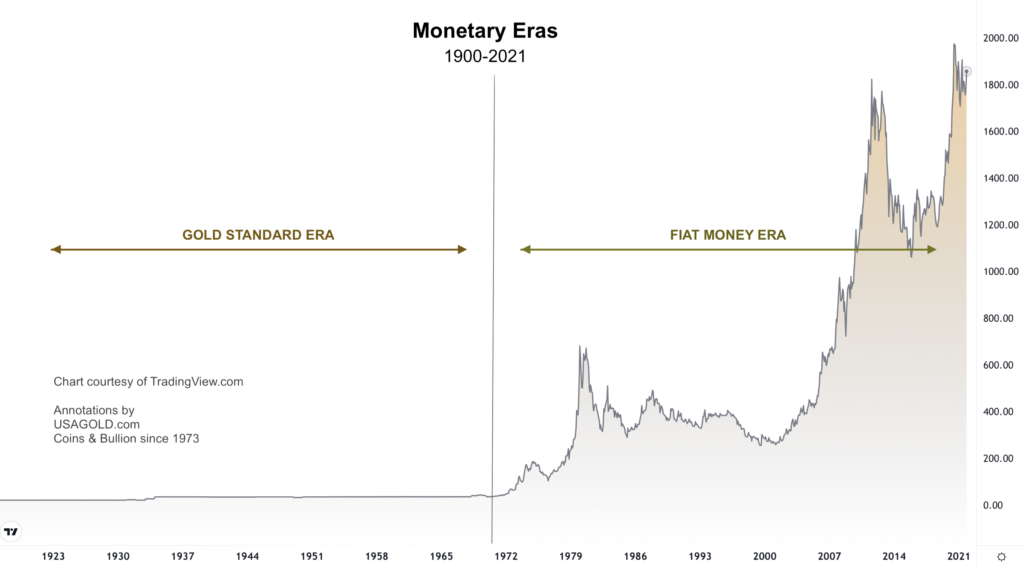

‘A bond issued by God’

That small group of investment bankers – those Tom Wolfe dubbed the Masters of the Universe – made its fortune trading U.S. Treasuries. It still plays the same role today it always has but no longer occupies the center stage for Wall Street’s bond market. Instead, that role now belongs to the Federal Reserve. Since the introduction of quantitative easing in 2008, it has built a $5.57 trillion stockpile of U.S. Treasuries – a holding equal to almost 20% of the nearly $29 trillion national debt. Even more troubling, it purchased a mind-boggling 60% t0 80% of the federal debt issued since 2010, according to a recent Wall Street Journal report.

“At 10:10 a.m. most workdays on Wall Street,” writes Liz McCormick in a recent Bloomberg column (under the unsettling headline, One Trader Calls the Shots in the Treasury Bond Market) officials at the Federal Reserve wade into the Treasury bond market. For the next 20 minutes, they proceed to snap up bonds of all shapes and sizes. They’re impervious to price moves, and they never sell. An indiscriminate bond-buying machine, they’ve now amassed a $5.5 trillion stockpile of the debt.” Wolfe’s Masters of the Universe have been replaced by one omnipresent, spectacularly powerful, and as it turns out, fickle Master of the Universe – America’s central bank.

“For almost two years,” says Gillian Tett, in a recent Financial Times editorial, “a frightening question has haunted the U.S. Treasury and Federal Reserve. No, this is not whether the Fed can engineer a smooth exit from quantitative easing; nor whether this is the right moment to switch the governor (and policy). The question I am referring to is whether the U.S. Treasuries market is robust enough to handle the shocks that might arise from those first two problems. For while the U.S. government bond market used to be considered to be the world’s most liquid and deep asset class, in March 2020 that cozy assumption was smashed apart.”

The bond market, in short, has become a much more dangerous place to park one’s money than it was in 1987 when Wolfe wrote Bonfire of Vanities. That vulnerability, in turn, has elevated the appeal of the bond market’s chief competitor for safe-haven capital – gold. As of the third quarter of 2021, the World Gold Council reports the strongest global year-to-date increase in gold coin and bullion demand since 2013, including a 31% year-over-year increase in U.S. demand.

London-based market analyst Charlie Morris says we should, in fact, view gold as a kind of bond in its own right. “In asking what kind of bond it is,” he says, “I came up with five answers:

• It is a zero-coupon because it pays no interest.

• It has a long duration because it lasts forever.

• It is inflation-linked, as historic purchasing power has demonstrated.

• It has zero credit risk, assuming it is held in physical form.

• It was issued by God.

That means gold is simply a zero-coupon, long-duration inflation-linked bond. It compensates you against past debasement and is impacted by the expectation of how rates and inflation will change in the future. It works.”

At the moment, an eerie calm prevails in the bond market. The question, however, is, will it last once the Fed withdraws its monumental support? Some economists think tapering will succeed simply because the federal government will require less financing now that the Covid-related spending storm has passed. Others are not convinced. As pointed out above, the Fed has purchased the lion’s share of the national debt issued since 2010. It was a significant player in the bond market long before the pandemic became a problem.

“Frankly,” asks Bloomberg’s Vince Cignarella, “given the biggest buyer of bonds since the financial crisis is slowing purchases, why would anyone else want them? The Fed not buying bonds is defacto selling.” In the same editorial linked above, Gillian Tett raises another possibility: “[W]hen markets awake from dreamland and reprice Treasuries, there is every chance we will see another nasty market jolt. Unless, of course, the Fed keeps acting as a trillion-dollar-a-day market maker of last resort. Which is not, of course, how free market finance is supposed to work.”

Click to enlarge

––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––